Infra

How has infrastructure been financed in the past? – Economics Observatory

Physical infrastructure – in the form of transport, energy, water and telecommunication systems – is an important catalyst for economic growth and development. Indeed, every £1 of infrastructure investment can raise GDP by 20p in the long run, a socio-economic return of around 20%, according to McKinsey Global Institute estimates.

Nevertheless, globally, there is a gap between projected investment and the amount needed to provide adequate global infrastructure. This ‘global infrastructure gap’ is estimated at $3.7 trillion a year, and few governments can fill this alone. In the current economic climate, many countries face major financial shortfalls due to weak external and fiscal balance sheets and elevated debt levels.

Indeed, government funds are increasingly squeezed to pay for healthcare, education and pension obligations, which can make investment in infrastructure unaffordable, despite the potential returns over the long run.

The period from 1880 to 1913 – popularly known as the first era of globalisation – can offer valuable lessons on financing large-scale infrastructure globally. At that time, infrastructure bond issuances were used to pay for large-scale infrastructure, something that governments today might wish to consider.

Historical background

The period of the late 19th and early 20th century is characterised as a time of high financial integration (when financial markets are closely linked together, whether across regions or countries). It was defined by large inflows of capital that came predominantly from Great Britain, and mushroomed prior to 1913 (Bordo and Meissner, 2010).

Overall, sovereign and railway securities comprised over two-thirds of the London Stock Exchange (66.8%), as Table 1 shows (Goetzmann and Ukhov, 2006).

Table 1: Capital invested by Great Britain overseas, December 1913

Source: Goetzmann and Ukhov, 2006

Railways expanded globally in these years as countries rushed to build networks for achieving both economic and strategic aims (see Figure 1).

For example, the vast Russian empire required railway links capable of moving the Tsarist army quickly and competently. Similarly, the ‘strategic’ railways on the north-west frontier of India were vital for imperial defence in British India (Otte and Neilson, 2012).

At the same time, capital-poor or capital-importing countries – such as Argentina – faced inadequate budgetary resources and shallow domestic capital markets (having a smaller domestic investor base and fewer choices of financial instruments).

As a result, they were unable to finance capital-intensive projects such as railways, which required large upfront costs for construction. This led capital-importing countries to look primarily for external resources and to borrow from abroad to finance large infrastructure projects. Private capital markets, such as the London Stock Exchange, were deep enough to finance such ventures (Coffman and Neal, 2013).

The railway network expansion and huge investor demand for railway construction led to sovereign and railway securities being the top-most avenues of British investment at the London Stock Exchange between 1880 and 1913.

Figure 1: Length of railway network

Source: Mitchell, 2005

Investing in the railway industry was a risky venture characterised by the expensive assets involved, which, once spent, weren’t recoverable (what economists refer to as high capital intensity and significant sunk costs).

The investments were therefore structured as emergent ‘build-operate-transfer’ (BOT) schemes, with both public and private shares in ownership and management.

In the BOT approach, the holder of the grants or concession – the concessionaire – retains a concession for a long-term fixed period (usually 30-40 years) for the development and operation of an infrastructure facility. The private infrastructure company builds, finances and operates the new infrastructure facility for a specific period. Ownership then reverts back, at no cost, to the public party – government, ministry or public agency (Xenidis and Angelides, 2005).

Public and private partnership in the ownership and management of railways was not the only way in which governments and corporations were linked. Public and private collaboration was also evident in railway securities, the primary instrument used to raise finance for railway construction.

Capital-poor countries faced with severe information asymmetries (where one party has more information than another) between buyers (investors) and issuers (borrowing governments and corporations), as well as shallow capital markets, attracted investment for building infrastructure networks through issuing infrastructure securities.

Railway securities were long-dated financial instruments that had a number of common features: the railway company for which the investment was being raised; the rate of interest offered on the investment; the underwriting firm issuing the security on behalf of the government; and the form of government support provided.

Railway securities were made attractive through offers of guaranteed returns, investment safety via sinking funds, defining collateral clauses and ensuring the marketability of securities (Kemmerer, 1916; Neumann, 2003).

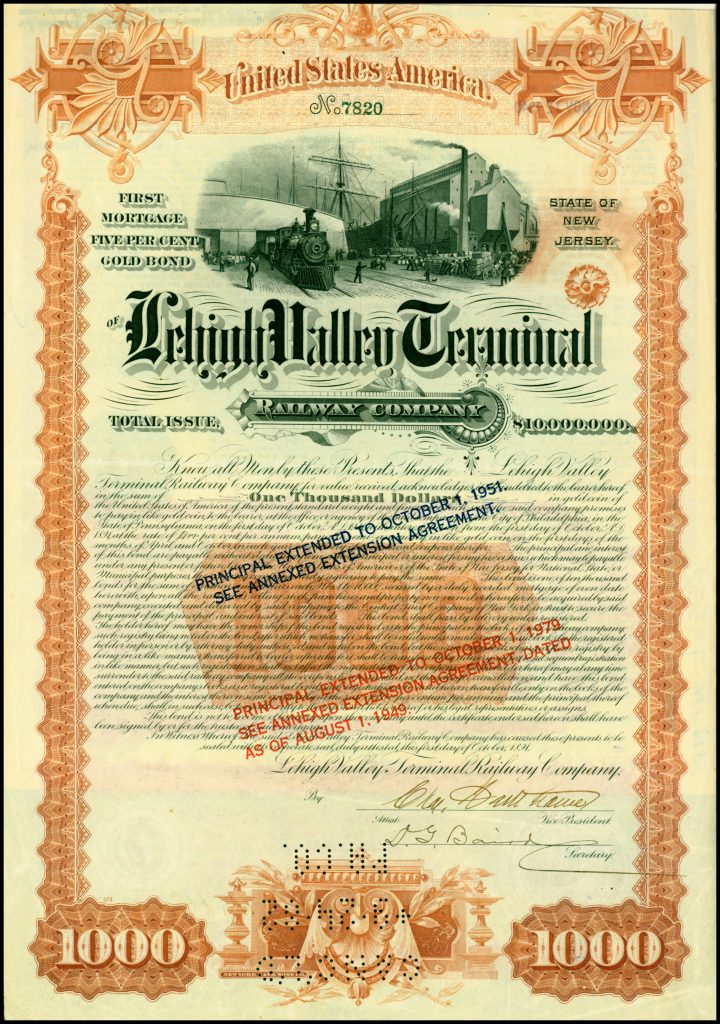

An example is the bond of the Lehigh Valley Terminal Railway Company in downtown Buffalo, New York. The terminal handled the Lehigh Valley’s passenger traffic in Buffalo until 1955 and hosted the Erie Railroad’s passenger trains from 1935 until 1951 (see Figure 2).

Figure 2: Railway bond of the Lehigh Valley Terminal Railway Company, 1891

Source: Wikimedia Commons

Governments offered various types of support to attract investment, such as land grants and subsidies. For example, the US government, looking to develop transport links in the west, offered railway companies the opportunity to earn land grants by actual construction of desired lines (Greever, 1951).

But the most important government support came in the form of guarantees. In the case of Indian railways, which formed a significant avenue of investment for the British public, the Indian government provided a guaranteed minimum interest with a participation in profits.

Despite the use of guarantees to attract investment, issuing governments used prestigious underwriters to signal to investors the creditworthiness of the project and to make the investment lucrative yet safe. The use of underwriters and innovative financial instruments contributed to the increase in overall market capitalisation of the London Stock Exchange and financial deepening of the British economy.

Investing public

It is also important to understand who was investing in railway securities. With the introduction of the Companies Acts of 1856 and 1862 and the emergence of limited liability – a form of legal protection for shareholders and owners – a growing number of less affluent people became investors in this period. These individuals began to own stocks and shares in railway companies (Rutterford et al, 2022).

The investing public was encouraged to diversify their risk through various media, including financial newspapers and investment periodicals. In this regard, newspapers like The Economist and the Financial Times were widely used for expert financial advice and to choose the securities offering higher risk-adjusted returns (Sotiropoulos and Rutterford, 2018).

The guaranteed stream of returns provided by railway companies attracted women and widows (Rutterford and Maltby, 2006). Women’s engagement with financial markets grew in the 19th century and they increasingly became investors, speculators, rentiers and members of private family-based companies.

Over time, financial trusts – largely what are known as closed-end funds – grew in importance. This was especially the case after the boom between 1887 and 1890, where 72 new trusts were floated on the London Stock Exchange.

Closed-end funds are a type of mutual fund that issues a fixed number of shares through an initial public offering (IPO) to raise capital for its initial investments. These sought to boost investment returns by earning a fee from underwriting new issues, investing in illiquid securities and specialising in various sectors, including railways in Latin American countries (Chambers and Esteves, 2014).

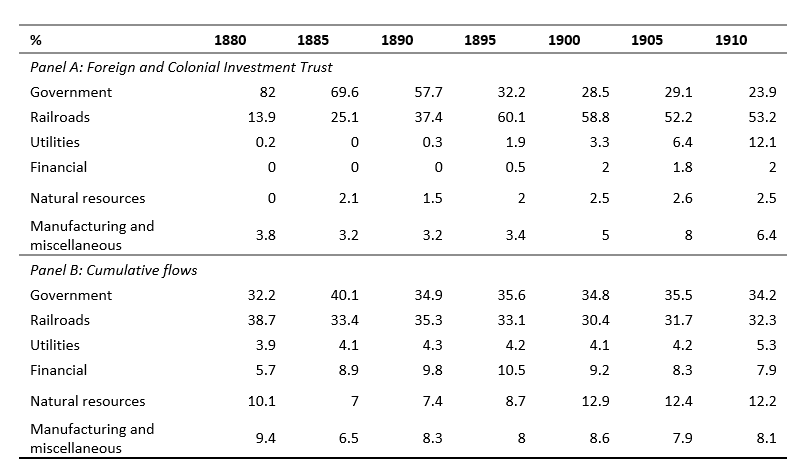

For example, Table 2 shows the sectoral allocation of the Foreign and Colonial Investment Trust, the oldest surviving closed-end fund today. Over a passage of 30 years (1880-1910), the trust increased its investment in railroads by 39%.

Table 2: Sectoral allocation of the Foreign and Colonial Investment Trust

Source: Chambers and Esteves, 2014

Infrastructure financing: lessons from the past

What lessons can the historical financing of infrastructure provide for policy-makers today? While much can be learned from this period, two lessons stand out: tapping long-term capital; and promoting project transparency for attracting investment.

First, governments can tap investors for long-term capital to promote green infrastructure, in the same way that trust funds invested in railway securities in the late 19th and early 20th centuries. Indeed, railways are an example of green infrastructure as they are energy efficient, and produce 70-80% less greenhouse emissions than cars, trucks or airplanes.

Working with investors that provide long-term capital ensures that debt maturities align with the long timeframes of infrastructure projects. This is important as railway projects are characterised by lengthy initial gestation periods, and it is only later that the benefits of the infrastructure can be realised.

A potential problem with this is that governments of emerging markets or developing countries face difficulties in accessing long-term capital due to political and demand risk. Infrastructure projects are long-term endeavours, and political interference, especially in emerging markets or developing economies, could endanger a predictable and safe revenue stream.

Further, demand risk poses a threat to debt repayment and equity returns (OECD, 2007). Governments can overcome this by exploring innovative models and products that minimise risk for long-term infrastructure projects with the support of multilateral institutions.

Similar to the past where prestigious underwriters listed railway securities on global stock exchanges – and their reputation depended on their sponsored issues performing well on the stock market – governments in developing countries today can benefit from multilateral institutions. For example, institutions such as the International Finance Corporation provide partial credit guarantees that can offer timely debt service payments up to a predetermined amount.

Assistance from multilateral institutions in the form of partial credit and stop-loss guarantees can improve the creditworthiness of projects and make them attractive for investment. In this regard, it is important to attract funds for well thought out, economically viable projects that create impact in the form of green growth. Investments in green infrastructure, especially transport, are good candidates.

The first era of globalisation also provides a lesson in the form of governments being transparent about railway projects. For example, an advertisement for the Uruguay Central and Hygueritas Railway Company of Montevideo, published in The Economist on 11 January 1873, elaborated the revenue earning potential of the railway stating:

‘The Central Uruguay Railway will […] run to Hygueritas where it will collect the vast and fertile provinces watered by the Uruguay and its tributaries, for conveyance by means of the Central Uruguay Railway to Montevideo, the capital of the Republic of Uruguay, and the best port of the River Plate’.

Large-scale infrastructure projects regularly published financial statements in the media to inform present and potential investors of performance at the design, build and operate phases of the infrastructure lifecycle.

Transparency can also be beneficial for attracting investment today. This is because private investors have faced significant barriers to investment in the form of a lack of available and reliable data for the expansion of large-scale infrastructure projects.

Conclusion

Sustainable infrastructure projects help to support economic activity and catalyse growth and development. History offers valuable lessons of where collaboration between public and private parties – in the form of public-private partnerships – have acted as a game-changer for financing large-scale infrastructure projects.

Government and private companies can combine their strengths to develop, design, finance and operate large-scale infrastructure projects soundly. Tapping long-term capital and promoting project transparency can prove beneficial in terms of attracting investment for mega infrastructure projects – those costing over £1 billion – to promote green growth and overall economic development.

Where can I find out more?

Who are experts on this question?

- Gareth Campbell

- Chris Colvin

- Bent Flyvbjerg

- Tehreem Husain

Author: Tehreem Husain

Image: The street railway journal, 1900, Wikimedia Commons

From Stadium to Screen: How Technology is Changing Sports Viewing

20/7/2024 Horse Racing Tips and Best Bets – Flemington, Flemington Cup day

Indian tech hub Karnataka state’s move to reserve jobs for locals not finalised, chief minister says

Financial picture dramatically improves for Shamrock Rovers in 48 hours with Sinclair Armstrong deal and European win

Our fashion editor’s favourite affordable bag is 20% off today

Jay Shah’s Big Decision Hovers Over Cricket’s Associate Member Directors Election

Budget shampoo that adds MAJOR volume boost is on sale for Amazon Prime Day: ‘Your hair feels fuller and thicker’

Being active on your commute lowers risk of disease and mental health

Tiger Woods cops brutal Open schedule as full Round 1 tee times revealed